News & Resources

Alexander Hutton is excited to present our 3rd quarter Northwest Market Update. In Q3 2024, the Northwest M&A market experienced a seasonal dip in deal volume, but a recent interest rate cut has sparked optimism for future growth. This quarter's report features an analysis on transaction counts and trends in the NW region as well as insightful commentary from our Managing Director, James Thompson.

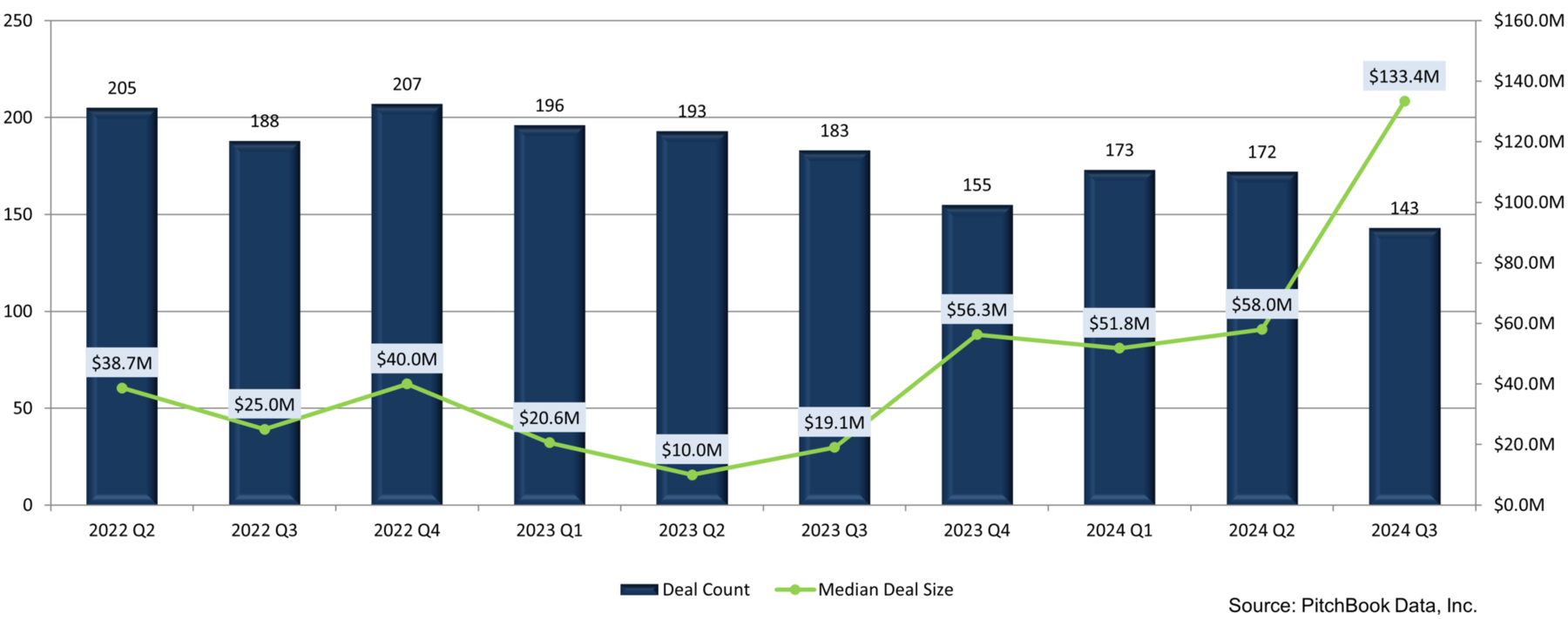

The State of the NW Market in Q3 2024

In the third quarter of 2024, the Northwest (WA, OR, ID, MT, WY & AK) M&A market saw a slight decrease in deal volume with 143 deals closed (down from 172 in Q2 2024). The decrease can be attributed to macroeconomic trends and seasonality. The third quarter typically sees a reduction in deal volume due to the summer months, as sellers and buyers spend more time away from the office. Additionally, buyers and sellers were anticipating a rate cut during Q3 of 2024, leading many to wait on the sidelines until the cost of debt fell. This rate cut eventually came in September, with the fed lowering interest rates by 50 bp. Economic uncertainty has started to dissipate, and there are many signs that persistent inflation is beginning to show signs of weakening.

Cost of Debt Reduced

In our Q2 market overview, we highlighted that PE funds are facing increased pressure to exit existing investments. Due to the high cost of debt, exiting portfolio companies has proven to be more difficult than anticipated. Over the past year, investors and business owners have been patient, waiting out periods of economic uncertainty, and conservatively allocating capital. With a 50 bp rate cut, and more to come as indicated by the Fed, we are expecting to see significant growth in deal volume over the next 12 months, as sellers and buyers start to decide to transact.

Concurrently, there has been ample activity in the private lending sector. Demand for private debt issuances has skyrocketed, leading investment banks scrambling to find ways to securitize these offerings and allow everyday investors to participate through a stock exchange. According to an article in the Wall Street Journal, investment giants such as Apollo, BlackRock, Capital Group, KKR and State Street are working to launch private credit ETFs which would allow anyone to tap into the $1.7T market of lending to corporations and consumers. This level of activity in the private lending space indicates there is more optimism from both borrowers and lenders about the direction of the economy.

Positive Outlook

The reduced cost of debt, coupled with anticipated rate cuts, has elicited a more positive outlook from business owners and capital allocators. According to an EY CEO Outlook Pulse survey of 1,200 executives, seven in ten of the CEOs surveyed shared an optimistic outlook for the economy. In Q3 of 2024, the U.S. economy in particular experienced wage growth, lower unemployment, resilient retail sales, rising business investment and increased consumer confidence. With these tailwinds, businesses will choose to be more aggressive with growth strategies which include increased investment and M&A. As investors become more confident about the state of the economy, the willingness to put capital to work and pay higher prices for quality companies will continue to rise.