News & Resources

This month, we are featuring the Business Services industry for our Market Update. "The combination of favorable interest rates and anticipation of business-friendly policies creates a fertile environment for M&A in the business services sector." See below for our full update which includes insights on the Business Services market as well as notable middle-market deals from Q3.

Market Commentary

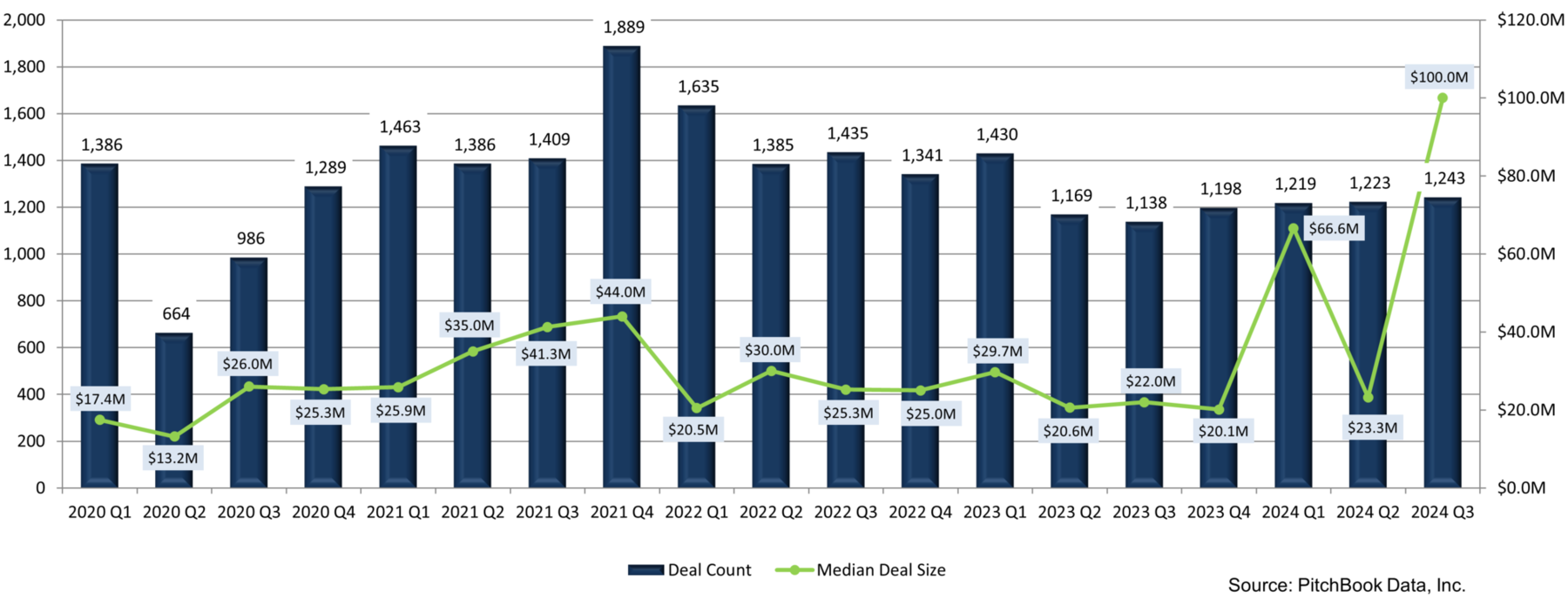

Transaction volume for the business services sector, which includes consulting services, technology services, professional services, and similar industries, remained steady during the third quarter of 2024. While deal volume continues to rebound from the contracted M&A market of 2023, activity remains below the record highs seen at the end of 2021. During that time, business services were in high demand as corporations looked to adapt quickly to the changing business landscape created by the pandemic. In the following years, demand for business services declined as companies began cost savings initiatives and looked to stockpile cash in response to persistent inflation and rising interest rates. In times of economic distress, outsourced business services are often some of the first expenses to be scrutinized by CEOs and CFOs.

As the Fed cut rates in 2024, with a half a point cut in September and a quarter point cut in November, we expect activity in the M&A market to respond positively as buyers utilize a lower cost of capital to bid competitively on businesses. Within the business services sector, we anticipate M&A deal volume to increase for the remainder of 2024 into 2025 as the following sector trends play out in the market:

- Technology service firms (including managed services, data analytics, cybersecurity, etc.) will remain attractive to both strategic buyers seeking to prioritize digital transformation and financial buyers looking to invest in business with recurring or predictable revenue.

- AI’s rise in recent months has increased business’s focus on AI adoption across industries to efficiently manage various business operations. Successful AI implementation often requires technical expertise from experienced technology consulting firms.

- The spike in transaction value in Q3 2024 was driven by the announcement of several large acquisitions across the industries within business services, such as EQT’s acquisition of Perficient for $3.16 billion and KKR’s acquisition of VMWare’s End-User Computing business for $4 billion.

Private Equity in Professional Services

In recent years, private equity firms have focused on stockpiling cash and developing new investment thesis, including in the professional services space. As of early 2024, global private equity dry powder (committed capital) reached a record high of $2.62 trillion. The professional services space is attractive to financial buyers due to the steady cash flow, high margins and increasing demand for digital and technology-driven services. For example, in an article published by the Wall Street Journal, it was reported that by the end of 2025, more than half of the 30 largest U.S. accounting firms will have sold an ownership stake to private equity investors, up from zero in 2020. Private equity has identified professional services as a highly fragmented market with tremendous upside and ROI upon consolidation. We expect this is just the beginning of an aggressive consolidation in this space and anticipate this new focus area to drive M&A growth within the sector.

Artificial Intelligence

Artificial intelligence is at the forefront of heavy investment into technology service companies, seen through an increase in AI-driven deals in the recent quarter. To keep pace with competition and provide advanced offerings to customers, companies are having to showcase market-leading A.I. services, often requiring outsourced services from specialized professional services firms for implementation. Additionally, many business service companies are approaching AI through an inorganic growth lens and establishing an A.I. vertical via acquisition rather than building out its own function. This is a major driver for M&A activity and should help drive continued growth in deal count within the business services sector.

In Conclusion

As we enter the final quarter of 2024, we expect to see continued strength in the business services M&A market, driven by strong tailwinds that include private equity’s focus on professional services, A.I. adoption and falling interest rates. Now that a period of economic uncertainty is behind us, businesses will look to the future and begin to re-engage many business services professionals to help fuel growth for years to come.